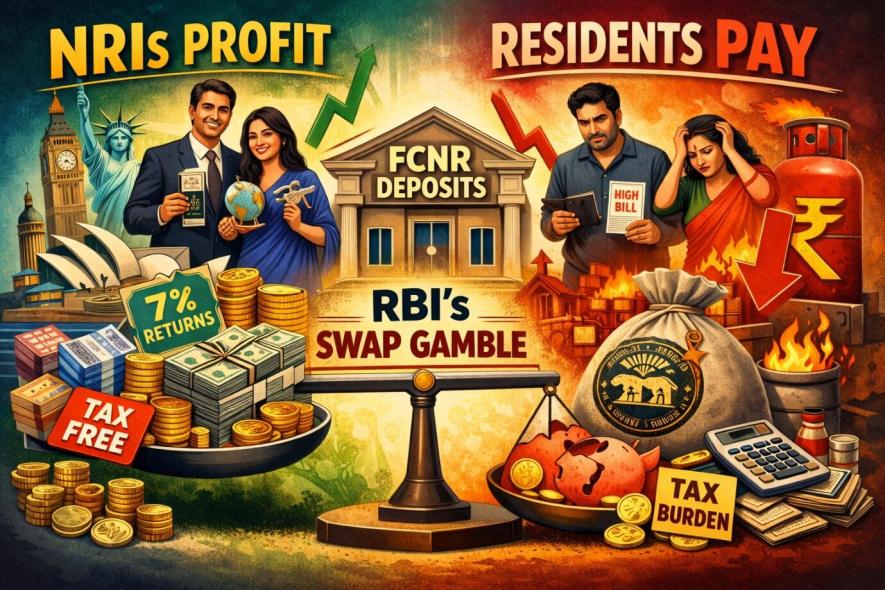

When NRIs Profit, Residents Pay: RBI’s Swap Gamble

India’s NRI (non-resident Indian) deposit story is a tale of shifting liabilities. In 1975, FCNR(A) placed the entire exchangerate risk on the Reserve Bank of India, shielding NRIs completely but burdening the central bank. By 1993, this unsustainable model gave way to FCNR(B), where banks managed deposits directly in foreign currency, reducing RBI’s exposure.

Three decades later, however, the swap facility has quietly reintroduced hidden support. Banks mobilise FCNR(B) deposits in dollars, pounds, or euros, then swap them with the RBI at fixed rates. The RBI absorbs hedging costs that would otherwise run 3–4% annually, enabling banks to offer NRIs globally unmatched returns — as high as 7.13%, and now up to 8% after the temporary removal of the interest rate cap.

The RBI’s reserves are not abstract; they are built from the taxes, exports, and savings of ordinary Indians. When those reserves subsidise foreign returns, residents silently pay the price. Their rupee deposits earn 6–7% in nominal terms but lose real value to depreciation, while NRIs flourish abroad.

This dynamic is more than economic; it is emotional. The pride of resident Indians is bruised when their own sacrifices fund the prosperity of others. A policy designed to stabilise the rupee externally weakens it internally, creating a paradox: the citizen at home pays for the prosperity of the citizen abroad.

The intent is clear — stabilisation and inflows — but the effect is doubleedged: a shortterm stabiliser that risks becoming a longterm subsidy. The question is not whether NRIs should benefit, but whether India can afford to do so at the cost of its own citizens’ wealth and dignity.

Mechanics of FCNR(B) and the Swap

How the Swap Works: Under the swap facility, banks mobilise FCNR(B) deposits in permitted currencies (dollar, pound, euro, Australian dollar, Canadian dollar). Instead of bearing hedging costs themselves, they enter into a swap with the RBI:

- Bank sells foreign currency to RBI and receives rupees at today’s exchange rate.

- Swap contract signed: Bank agrees to buy back the same currency later at the same rate.

- RBI absorbs the hedging cost (normally 3–4% annually).

- Banks pass the benefit to NRIs by offering 6–7% interest, far higher than US/European CDs.

- At maturity: NRI gets back principal + interest in foreign currency, shielded from rupee depreciation.

Who Really Pays:

NRIs: Premium returns, no currency risk.

- Banks: Protected, no hedging expense.

- RBI: Shoulders hedging cost.

- Residents: Indirectly pay, because RBI’s reserves are built from their taxes, exports, and national savings.

Source: RBI Circular (July 2022, extended in 2026): “Banks are permitted to enter into swap transactions with RBI to mobilize FCNR(B) deposits.” Economic Times / Business Standard: “RBI’s swap facility allows banks to offer higher FCNR(B) rates by absorbing hedging costs.”

Comparative Charts

Numbers reveal the imbalance more starkly than words. As of June 2026, FCNR(B) deposit rates offered by Indian banks stand well above comparable US Certificate of Deposit (CD) rates, highlighting the premium gap.

FCNR(B) Deposit Rates (3–5 years, June 2026)

- AU Small Finance Bank: 7.10%

- Equitas Small Finance Bank: 7.13%

- Yes Bank: 6.75%

- IndusInd Bank: 6.50%

- HDFC Bank: 6.00%

- ICICI Bank: 6.00%

- Axis Bank: 5.75%

- State Bank of India (SBI): 5.50%

- Postcap removal (valid until Sept 2026): Banks may now offer up to 8.00%.

US CD Rates (1 year, June 2026)

- JPMorgan Chase: 3.20%

- Bank of America: 3.45%

- Goldman Sachs (Marcus): 4.00%

- Wells Fargo: 3.25%

- Citibank: 3.40%

The Premium

FCNR(B) deposits consistently offer a 200–300 basis point premium over US CDs. With the RBI’s temporary removal of the interest rate cap, the premium has widened to 400–500 basis points, making NRI deposits globally unmatched.

Sources: Business Standard / Economic Times: “FCNR(B) deposits now offer a 200–300 basis point premium over U.S. CDs, thanks to RBI’s swap facility.”

Newspaper report, Kolkata dateline (June 2026): “RBI removes cap on NRI deposit rates until September; some banks may offer up to 8% to boost ALM profiles.”

Resident Indians’ Burden

The swap facility may look like a stabiliser on paper, but its hidden costs fall squarely on resident Indians. With the RBI’s temporary removal of the interest rate cap until September 2026, those costs have widened further, deepening the imbalance between residents and NRIs.

Inflationary Impact: When the RBI deploys reserves to absorb hedging costs, its ability to fight inflation weakens. Depreciation of the rupee raises the cost of imports — fuel, food, medicines — all of which feed directly into everyday prices.

Savings Erosion: Resident Indians earn 6–7% on rupee fixed deposits. Yet with the rupee depreciating by 4–5% annually, those returns vanish in real terms. What appears as a gain in nominal numbers is wiped out by currency weakness, leaving the ordinary saver with shrinking purchasing power. As shown in Section 2, deregulation widened the premium gap to 400–500 basis points, with NRIs enjoying ceilingfree rates of up to 8% shielded from depreciation.

Pride Hurt

There is an emotional dimension too. Citizens see their own savings erode while NRIs are offered premium yields subsidized by national reserves. The paradox is stark: the resident pays for the prosperity of the nonresident. Pride is bruised when the nation’s wealth sustains foreign gains while domestic savers remain exposed. The deregulation episode sharpens this paradox — residents remain capped by inflation, while NRIs are actively courted with globally unmatched yields.

Source: RBI Annual Report: “Depreciation of the rupee has contributed to inflationary pressures and erosion of real returns on domestic deposits.”

- Mint analysis: “Resident savers earning 6–7% on rupee deposits often see their real returns wiped out by currency depreciation, even as FCNR(B) deposits remain shielded.”

NRI Gains and Obligations

The swap facility has created a rare alignment of advantages for NRIs. While resident Indians see their rupee savings eroded, NRIs enjoy a shielded position that combines high yields with currency protection. With the RBI’s temporary removal of the interest rate cap until September 2026, these advantages have become even stronger.

Gains for NRIs

Premium Returns: As shown in Section 2, FCNR(B) deposits currently offer yields far above U.S. CDs, widened further by deregulation.

- Currency Shield: Deposits remain in foreign currency, fully protected from rupee depreciation.

- TaxFree in India: Interest earned on FCNR(B) deposits is exempt under Section 10(15)(iv)(fa) of the Income Tax Act.

- Repatriability: Both principal and interest are fully repatriable, giving NRIs flexibility to move funds across borders.

Obligations Abroad

NRIs who are US persons must report FCNR(B) deposits under FATCA and FBAR.

- FATCA (Foreign Account Tax Compliance Act): A U.S. law requiring foreign financial institutions (including Indian banks) to report information about accounts held by U.S. taxpayers. NRIs who are U.S. persons must disclose their FCNR(B) deposits and other foreign accounts to the IRS. Even if interest is taxfree in India, it may still be taxable in the U.S.

- FBAR (Foreign Bank Account Report): A separate reporting requirement under the Bank Secrecy Act.

- U.S. persons must file an annual FBAR (FinCEN Form 114) if the total value of their foreign accounts exceeds $10,000 at any time during the year.

- Noncompliance can lead to severe penalties, including fines and possible criminal charges.

In short: FATCA is about tax compliance, FBAR is about financial transparency. Together, they ensure U.S. taxpayers cannot hide income or assets abroad.

- European Union / CRS Framework: Automatic exchange of information under CRS means deposits are disclosed to tax authorities abroad.

- Gulf Countries: NRIs in taxfree jurisdictions (UAE, Saudi Arabia, Qatar, etc.) enjoy the full benefit — taxfree in India and no tax abroad.

The Contrast

- NRIs in the West: Gain premium returns but face compliance and taxation abroad.

- NRIs in the Gulf: Enjoy the “perfect arbitrage” — high yields, currency protection, and no tax obligations.

- Residents in India: Earn nominal returns eroded by inflation and depreciation, while their reserves subsidize NRI gains.

- Deregulation sharpens this contrast: residents remain capped by inflation, while NRIs are actively courted with globally unmatched yields.

Sources: Income Tax Act, Section 10(15)(iv)(fa): “Interest on FCNR(B) deposits is exempt from tax in India.”

- IRS FATCA Guidance: “U.S. persons must report foreign financial accounts, including deposits held abroad.”

- OECD CRS Framework: “Participating jurisdictions exchange information on nonresident financial accounts.”

Policy Paradox

The Reserve Bank of India’s swap facility embodies a paradox in financial governance. Its stated purpose is straightforward: to stabilize the rupee, attract foreign inflows, and reassure markets during volatility. Yet in practice, the mechanism has evolved into a hidden subsidy for diaspora wealth, borne indirectly by resident citizens. This paradox has deepened with the RBI’s temporary removal of the interest rate cap until September 2026, allowing banks to offer globally unmatched yields.

Policy Intentions

The RBI’s intent is not misplaced. By absorbing hedging costs, it enables banks to mobilize foreign currency deposits quickly, strengthening reserves and signalling stability to investors and rating agencies. Presented as a technical measure rather than a subsidy, the swap preserves policy credibility. The cap removal is justified as a liquidity and assetliability management (ALM) measure, but it reinforces the perception that policy is tilted toward chasing foreign dollars rather than protecting domestic savers.

Unintended Consequences

Alongside these intentions lie consequences that remain largely invisible:

- Redistribution of Wealth: NRIs enjoy premium returns, banks are shielded from risk, while residents pay through reserves and inflation.

- Return of Liability: A burden that FCNR(B) was designed to remove has quietly returned in disguised form, reintroducing dependence on the central bank.

- Moral Hazard: Banks lean on RBI’s protection rather than managing risk themselves. Deregulation sharpens this hazard — banks now compete to offer ceilingfree rates, knowing RBI’s stance will backstop their risk appetite.

The Paradox in Practice

As a shortterm stabiliser, the swap succeeds in attracting inflows and calming markets. Over time, however, it entrenches a system where stabilization morphs into subsidy, reversing the very purpose of FCNR(B). The removal of the interest rate cap illustrates how a temporary stabilizer can evolve into a structural bias — privileging diaspora wealth while leaving resident savers exposed.

Sources: RBI Circular (July 2022, extended in 2026): “Banks are permitted to enter into swap transactions with RBI to mobilize FCNR(B) deposits.”

- Economic Times analysis: “While the swap facility stabilizes the rupee in the short term, it effectively subsidizes NRI deposits at the expense of resident savers.”

Citizen’s Toolkit

The paradox of FCNR(B) swaps cannot be left as a mere observation. Citizens need tools — reforms, safeguards, and accountability mechanisms — to ensure that stabilization does not become subsidy. With deregulation widening the premium gap, the urgency for citizencentric reforms has only grown.

Practical Reforms

- Transparency in RBI Swaps

- Publish monthly data on swap volumes, hedging costs absorbed, and reserve impact.

- Citizens deserve visibility into how national savings are deployed.

- Resident Saver Protection

- Introduce inflationindexed savings instruments to safeguard real returns.

- Offer taxfree status on select longterm resident deposits, mirroring FCNR(B) benefits.

- Consider a “parity clause”: if NRI deposit caps are lifted, resident deposits should also receive enhanced protection or incentives.

- Bank Accountability

- Require disclosure of the share of FCNR(B) deposits mobilised under swaps versus markethedged deposits.

- Banks offering ceilingfree rates should explain how inflows affect their ALM profiles, restoring risk discipline and citizen trust.

- Rating Agency Oversight

- Global rating agencies often applaud inflows without noting hidden subsidies.

- India should demand disclosure of how such inflows are assessed, preventing “rating shopping” and manipulation.

- Citizen Representation

- Establish consultative forums where citizen voices are heard in policy decisions affecting savings and reserves.

- Financial governance must be citizencentric, not just marketcentric.

- Episodes of cap removal should be debated publicly, ensuring residents’ interests are not sidelined in the chase for foreign inflows.

Sources: RBI Annual Report (2025–26): “Transparency in foreign exchange operations is essential to maintain public trust in reserve management.”

- Business Standard editorial: “Resident savers need inflationprotected instruments to offset the hidden subsidy embedded in FCNR(B) swaps.”

Closing Statement

India cannot become an economic giant by leaning on temporary subsidies or hidden support. The RBI’s swap facility and cap removal may attract inflows, but lasting strength requires weaving shortterm stabilizers with longterm reforms. A currency earns global respect — tradable abroad and trusted at home — only when backed by strong fundamentals: disciplined fiscal policy, diversified exports, reduced import dependence, and transparent disclosure of reserve data. Reserves must serve both citizens and markets, ensuring that India’s financial governance is anchored in resilience, credibility, and dignity.

The writer is a CAIIB (Certified Associate of the Indian Institute of Banking and Finance), has 37 years of work experience in the private sector and in a nationalised bank, and is the ex-All India Deputy General Secretary of the All India Bank Officers’ Confederation.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.