Rajesh Exports -- II: Alleged Accounting Mirage & Forensic Unfolding

The earlier article examined SEBI’s sudden interim order that shook confidence in Rajesh Exports. It highlighted how opacity in corporate disclosures can destabilise citizen trust in financial governance. This article turns the lens to the forensic details — tracing how alleged accounting practices at Rajesh Exports left even bankers, auditors, and seasoned finance professionals bewildered.

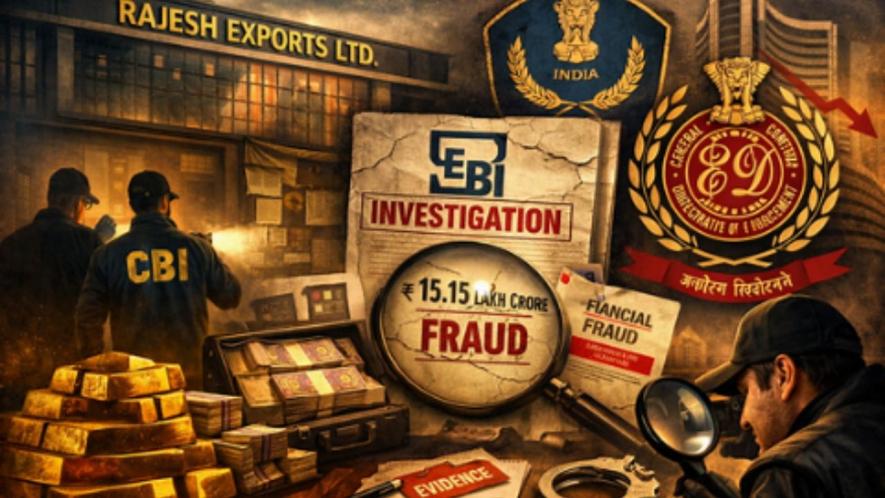

Until early June 2026, Rajesh Mehta and his company were little known outside bullion circles. Rajesh Exports operated quietly, projecting itself as a global gold refiner through its Swiss arm, Valcambi SA, but remained absent from mainstream financial debate. That obscurity ended abruptly when SEBI’s order alleged inflated consolidated revenues of ₹15.15 lakh crore between FY21 and FY25. As reported by NDTV Profit, The Indian Express, and Firstpost, the regulator also flagged receivables outstanding for years, auditor noncooperation, and layering of fund flows — anomalies that could no longer remain concealed.

The surfacing of these allegations transformed Rajesh Exports from a niche bullion player into a headline controversy. Bankers and auditors who had never scrutinised the company closely, were suddenly confronted with figures that defied logic. The company’s rebuttal — that SEBI merely confused EBITDA with revenue — only deepened the debate. A forensic lens is now essential to cut through the fog and examine what really happened.

The Sudden Surfacing

For years, Rajesh Exports remained a quiet bullion refiner, its global presence anchored in Switzerland through Valcambi SA but largely absent from India’s mainstream financial debate. That low profile ended abruptly on June 3, 2026, when SEBI issued its interim order. Overnight, the company moved from obscurity to the centre of a national controversy.

As reported by NDTV Profit, The Indian Express, and Firstpost, SEBI alleged that Rajesh Exports had inflated consolidated revenues by ₹15.15 lakh crore between FY21 and FY25. The order also pointed to unresolved receivables, auditor silence, and complex fund flows. What had long remained concealed was suddenly exposed leaving the financial community scrambling to interpret the scale of the alleged anomaly.

Read Also: Rajesh Exports: India’s Global Gold Giant Under Citizen Scrutiny

The market reaction was immediate and unforgiving. Rajesh Exports’ shares hit the lower circuit, trapping retail investors who could not exit. Institutional exposures, including LIC, saw wealth eroded in a matter of hours. For citizens, the scandal was not just about accounting entries — it was about trust. How could a company so little known outside bullion circles, suddenly be accused of inflating revenues on a trillionrupee scale? The surfacing of SEBI’s order transformed Rajesh Exports into a symbol of alleged opacity in India’s financial governance.

The Allegation

SEBI’s interim order did more than thrust Rajesh Exports into the spotlight — it laid out a set of detailed allegations that challenged the credibility of the company’s financial reporting. The order flagged three core anomalies: receivables that remained outstanding for more than two years, auditors who allegedly failed to cooperate with SEBI’s queries, and layering of fund flows that obscured transparency. Shareholder complaints had already raised concerns about the mismatch between reported revenues and actual cash inflows, and SEBI’s findings gave those concerns regulatory weight.

Taken together, these elements painted a troubling picture: a company projecting scale without substantiating it. For regulators, the issue was not about technical definitions but about whether Rajesh Exports had misled investors and institutions by presenting a mirage of revenues. The forensic spotlight was now firmly on the company’s accounting practices.

The Defence

In response to SEBI’s interim order, Rajesh Exports moved swiftly to defend its financials. As reported by NDTV Profit on June 6, the company denied inflating revenues and claimed the regulator had simply confused Valcambi SA’s EBITDA with consolidated revenue. Management emphasised that no adverse findings had been made against it and expressed confidence that the matter would be resolved once documents were submitted.

This rebuttal was framed as a matter of technical misinterpretation rather than deliberate malpractice. By presenting the issue as “just confusion,” Rajesh Exports sought to reassure investors and institutions that the anomaly was definitional, not fraudulent. The defence positioned the controversy as a misunderstanding, buying time and softening the tone of regulatory scrutiny.

Yet, for many observers, the explanation appeared more rhetorical than substantive. The claim of confusion raised further questions rather than resolving them, setting the stage for forensic analysis of whether the defence could withstand basic accounting logic.

The Forensic Catch

Rajesh Exports’ defence — that SEBI confused Valcambi’s EBITDA with consolidated revenue — collapses under basic accounting logic. EBITDA, by definition, is derived from revenue after deducting operating costs. It can never exceed revenue. If SEBI had indeed mistaken EBITDA for revenue, the consolidated topline would have appeared smaller, not larger. Yet, Rajesh Exports reported revenues ballooning to ₹15.15 lakh crore between FY21 and FY25. This contradiction makes the defence implausible.

The forensic catch lies in how Valcambi’s gold processing was allegedly reported. In Switzerland, Valcambi’s accounts show only the refining margin — the modest fee earned for turning raw gold into bars. In India, however, Rajesh Exports is alleged to have treated the entire value of bullion flows passing through the refinery as revenue.

In simple terms, instead of recording just the service fee, the company booked the full worth of the gold itself. This accounting choice inflated the consolidated topline, creating the optics of a trillionrupee exporter. By reframing the anomaly as “EBITDA confusion,” the company sought to shift blame to interpretation rather than intent. Yet, the forensic reality suggests that gross bullion flows were presented as revenue — a practice that misrepresents scale.

The receivables mismatch removes the curtain from this illusion. Shareholder complaints, as reported by NDTV Profit, highlighted trade receivables outstanding for more than two years. Genuine revenues should have translated into cash inflows, but instead receivables piled up without resolution. Operatively, receivables were booked as assets, inflating the balance sheet, but these did not behave like real claims.

SEBI’s order flagged auditor noncooperation and layering of fund flows — suggesting that receivables were shuffled across subsidiaries to create the appearance of settlement without genuine liquidation. This confusion around receivables is the forensic smoking gun: revenues without cash are a mirage, receivables without resolution are placeholders for opacity, and auditor silence allowed these placeholders to masquerade as legitimate.

Revenue & Profit Narration (FY21–FY25)

Across five years, Rajesh Exports reported consolidated revenues that added up to ₹15.15 lakh crore. Year by year, the topline hovered in the range of ₹2.5–3 lakh crore in FY21, rose slightly to about ₹2.8–3 lakh crore in FY22, edged higher to ₹3.0–3.2 lakh crore in FY23, climbed again to ₹3.2–3.5 lakh crore in FY24, and finally peaked at ₹4.23 lakh crore in FY25. Yet, the Indian standalone entity in FY25 showed only ₹7,027 crore of revenue, with profits taxed domestically on that modest base.

Taxation Cheat Sheet

The forensic catch extends to taxation. By offsetting inflated sales with equally inflated costs or receivables that never converted into cash, Rajesh Exports could show massive scale without triggering higher tax bills. The umbrella planning worked as follows:

- Treat gross gold movements as revenue in consolidated accounts → artificially enlarge topline.

- Keep standalone Indian revenue modest → limit domestic tax liability.

- Attribute most revenue abroad → profits taxed only on margins in Switzerland.

- Outcome → optics of a trillionrupee exporter, without proportionate taxation anywhere.

Source: NDTV Profit, “Just Confusion? Rajesh Exports Defends Financials After SEBI Flag, Denies Inflating Revenue” (June 6, 2026).

Chain of Negligence

The forensic anomalies — inflated bullion flows booked as revenue, unresolved receivables, and the taxation cheat sheet — do not exist in isolation. They point to a chain of negligence across institutions that were meant to safeguard financial integrity.

Public sector Canara Bank sits at the first link. As the sole lender to Rajesh Exports, its credit appraisal and monitoring should have pierced the receivables illusion. Receivables outstanding for more than two years are not assets but warning signals. Yet, Canara Bank relied on audited balance sheets and accepted receivables at face value, exposing itself to repayment risk. In banking practice, ageing analysis and debtor confirmations are standard; their absence here shifts the onus of scrutiny squarely onto the lender.

Auditors form the second link. SEBI’s order noted noncooperation and layering of fund flows. By certifying accounts despite receivables stagnation and inflated consolidation, auditors allowed opacity to masquerade as legitimacy. Their silence converted anomalies into accepted financial statements, misleading both lenders and investors.

Regulators are the third link. SEBI eventually flagged the anomalies, but only after years of inflated reporting. The delay meant that investors, banks, and even public institutions like LIC were exposed to distorted financials. Regulatory vigilance came late, allowing the illusion to persist.

Management completes the chain. By booking gross bullion flows as revenue, layering receivables, and structuring taxation to minimize liability, Rajesh Exports engineered the optics of scale while evading scrutiny. The defence of “EBITDA confusion” collapses under forensic logic, revealing intent to misrepresent rather than mere misinterpretation.

Together, this chain of negligence shows how each actor’s lapse compounded the others. The forensic catch exposed the mechanics; the chain of negligence reveals the accountability. For citizens, the impact is clear: when institutions fail in scrutiny, the burden of fraud shifts onto depositors, policyholders, and taxpayers.

Citizen Impact

The Rajesh Exports episode is not confined to boardrooms or balance sheets. Its impact has spilled directly into the lives of ordinary citizens and institutions. Retail investors who trusted the company’s reported revenues found themselves trapped in lower circuits, unable to exit as share prices collapsed. Policyholders, through LIC’s exposure, saw their premiums eroded — a silent transfer of risk from corporate promoters to the public. Banks, relying on audited balance sheets, extended credit that may now be distressed, exposing depositors and taxpayers to hidden costs.

As reported by NDTV Profit in its coverage “Just Confusion? Rajesh Exports Defends Financials After SEBI Flag, Denies Inflating Revenue”, the company’s defence of “just confusion” has only deepened uncertainty. If seasoned bankers and auditors are left bewildered, what chance do ordinary investors have of understanding the scale of alleged anomalies?

The opacity in globallocal consolidation has created a fog in which citizens cannot distinguish genuine sales from paper entries. This confusion is not incidental — it is symptomatic of systemic governance failure.

The citizen impact is, therefore, twofold. First, wealth erosion: savings diminished, premiums exposed, and deposits put at risk. Second, trust erosion: confidence in auditors, regulators, and institutions shaken. When every safeguard fails — management allegedly inflating sales, auditors signing off despite mismatches, banks relying blindly, regulators acting late — the burden falls squarely on citizens. The Rajesh Exports case is thus not just about corporate misrepresentation; it is about the systemic failure to protect the public from opacity and negligence.

Closing Statement

Whether this is alleged confusion or alleged malpractice, the Rajesh Exports case demonstrates how opacity in globallocal consolidation can mislead even seasoned finance professionals. Courts and regulators are unlikely to be fooled — but citizens must demand clarity before trust can be restored.

The episode leaves a deeper question hanging: why do frauds of such scale keep recurring in India’s financial markets, and why is it that retail investors suffer most at the hands of regulators and manipulators? From IL&FS to Yes Bank, and now Rajesh Exports, the script appears familiar — management allegedly inflates, auditors sign off, banks rely blindly, regulators act late, and citizens pay the price.

The challenge now is not only to resolve this case but to rebuild confidence in India’s financial governance. What role will the government and institutions play to ensure accountability? Will reforms strengthen auditor independence? Will regulators act faster to prevent opacity from festering? Will banks and insurers adopt stricter due diligence before exposing public funds?

The broader effect on India’s economy cannot be ignored. If trillionrupee anomalies continue to surface, investor confidence will erode, capital inflows may slow, and the credibility of India’s growth story could be questioned.

Whether this translates into measurable impact on GDP is still a developing story. But the perception gap is already visible: citizens wonder how an economy aspiring to global leadership can repeatedly be shaken by alleged accounting mirages.

The Rajesh Exports case is, therefore, more than a corporate controversy. It is a test of India’s governance architecture — of whether opacity will be pierced by accountability, and whether citizens will finally see reforms that protect their wealth and restore trust in the nation’s financial future.

The writer is a CAIIB (Certified Associate of the Indian Institute of Banking and Finance), has 37 years of work experience in the private sector and in a nationalised bank, and is the ex-All India Deputy General Secretary of the All India Bank Officers’ Confederation.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.