Energy Geopolitics and US-BRICS War: Who’s Next After Iran, Venezuela, Syria?

US - Israeli airstrikes on Iran. via Telegram

The 21st century has entered a phase in which energy geopolitics, sanctions regimes, and technological rivalry converge into what increasingly resembles a structural confrontation between a declining unipolar hegemon and an emergent multipolar bloc. The pattern is unmistakable: Iran under relentless pressure; Venezuela subjected to sanctions and regime-change attempts; Syria devastated by proxy war and economic strangulation.

The broader question, therefore, arises: after Iran, Venezuela, and Syria, which state becomes the next arena of coercive containment? This is not a matter of episodic crises. It reflects a deeper transformation in the material foundations of global power.

Structural Crisis of Post-1945 Order

Since 1945, the international system has rested upon three interlocking pillars:

- Dollar centrality in global reserves and trade settlement.

- US military primacy across maritime chokepoints and alliance networks.

- Institutional dominance through IMF, World Bank, and Bretton Woods architecture.

Today, each of these pillars confronts mounting strain.

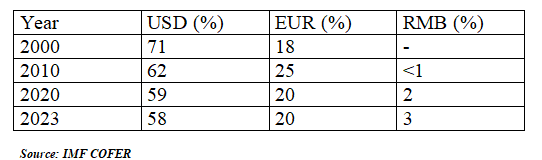

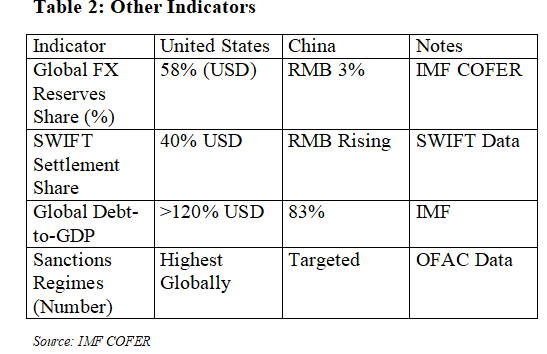

The dollar still constitutes roughly 58% of global foreign exchange reserves (IMF COFER data), but its share has gradually declined from over 70% at the turn of the century. Diversification toward the euro, renminbi, and gold—though incremental—signals a search for hedging mechanisms against sanctions risk and asset freezes.

The freezing of sovereign reserves in recent conflicts marked a qualitative turning point. Financial infrastructure—once assumed to be politically neutral—has been weaponised. This has profound implications for states in the Global South, many of which now perceive monetary dependence as strategic vulnerability.

The crisis is not purely diplomatic; it is structural. Advanced financialised capitalism in the US faces internal contradictions: high public debt levels (approaching $38 trillion against a GDP of roughly $30 trillion), deindustrialisation in key sectors, and reliance on financial expansion rather than productive renewal.

When profitability in the real economy stagnates, capital migrates into speculative instruments—debt, derivatives, and asset inflation—generating fragility beneath apparent prosperity. In such conditions, geopolitical coercion becomes an instrument of economic management.

Iran, Venezuela, Syria: Energy as Strategic Target

Iran, Venezuela, and Syria share a defining characteristic: their geopolitical centrality to energy routes, oil reserves, or regional connectivity.

Iran commands proximity to the Strait of Hormuz, through which a significant portion of global oil shipments pass. Venezuela possesses some of the world’s largest proven oil reserves. Syria sits at the crossroads of pipeline corridors linking West Asia to the Mediterranean.

These states are not randomly targeted; these are structurally positioned within the global energy architecture.

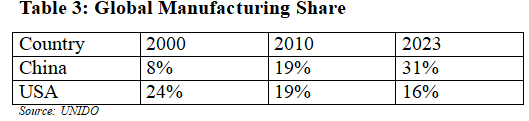

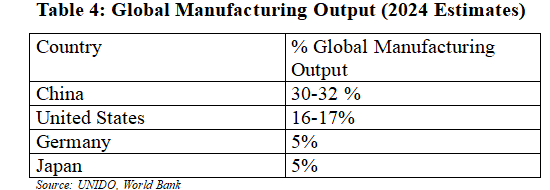

Energy remains the indispensable substrate of industrial civilisation. Control over energy flows reinforces monetary dominance, while industrial supremacy depends upon uninterrupted access to oil, gas, and strategic minerals. In a world where China has become the largest manufacturing economy—accounting for over 30% of global manufacturing output (UNIDO data)—energy security is inseparable from geopolitical competition.

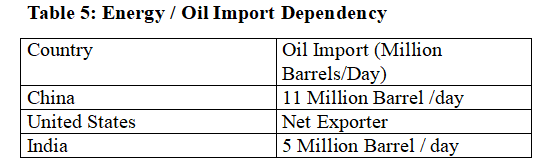

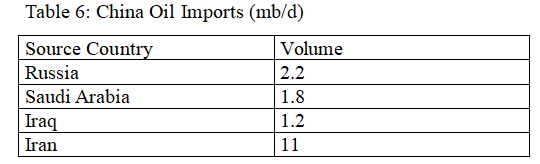

China imports roughly 11 million barrels of oil per day, drawing supplies from Russia, West Asia, and beyond. India imports approximately 5 million barrels per day. Energy corridors linking Eurasia thus intersect directly with BRICS economies. Any disruption in these corridors reverberates through industrial output, inflation, and strategic planning.

From this perspective, confrontation with Iran is not merely regional; it intersects with the broader containment of alternative Eurasian integration.

The USA–BRICS Contradiction

The principal contradiction of the current conjuncture lies between:

- A historically dominant finance-capital power seeking to preserve unipolar leverage;

- An emerging industrial-technological bloc seeking structural reconfiguration of global governance.

The US retains overwhelming military superiority and deep financial markets. China, however, commands expansive manufacturing capacity and increasingly sophisticated technological ecosystems. Russia wields energy leverage and strategic depth. India, Brazil, and South Africa navigate complex alignments while pursuing strategic autonomy.

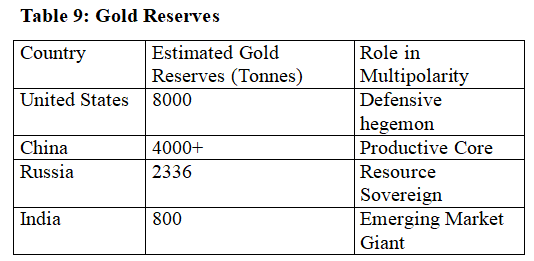

The BRICS initiatives—local-currency settlements, development finance mechanisms, and gold accumulation—reflect pragmatic hedging rather than abrupt systemic rupture. Yet even incremental diversification challenges the exclusive centrality of the dollar-based order.

The US has responded through multiple instruments:

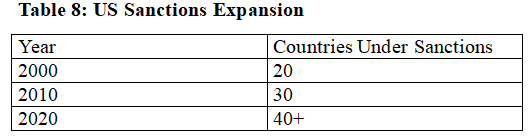

- Expanded sanctions regimes (over 40 countries under some form of sanctions in recent years);

- Semiconductor export controls;

- Investment restrictions;

- Alliance consolidation in Europe and the Indo-Pacific.

This confrontation transcends ideology. It concerns the material architecture of global power: supply chains, rare earth minerals, AI infrastructure, and maritime routes.

Militarisation and Alliance Consolidation

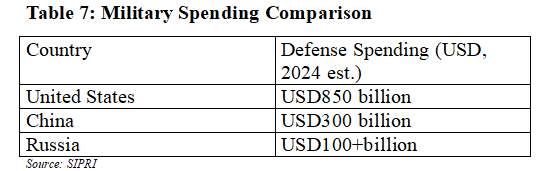

Military expenditures reveal structural asymmetry. The US allocates over $800 billion annually to defence—exceeding the combined spending of several major powers (SIPRI data). NATO expansion and Indo-Pacific alignments represent institutional adaptation to shifting power balances.

Direct great-power war remains avoided, but proxy conflicts proliferate. Sanctions have evolved into instruments of economic warfare, blurring the line between financial policy and strategic coercion.

In this environment, Iran, Venezuela, and Syria appear less as isolated conflicts and more as nodes in a broader strategy of containment directed at alternative energy and financial networks.

The central strategic logic is clear: prevent the consolidation of a multipolar system capable of bypassing Western-dominated financial and energy infrastructures.

Financialisation and Industrial Rebalancing

The US confronts a structural paradox. Monetary dominance persists, yet manufacturing share has declined from roughly 24% of global output in 2000 to approximately 16% today. China’s share rose from 8% to over 30% during the same period.

Industrial policy has, therefore, returned to Washington’s agenda—semiconductor subsidies, reshoring initiatives, infrastructure programs. The rhetoric of free markets has yielded to strategic planning.

Yet reindustrialisation under geopolitical fragmentation risks intensifying global rivalry rather than restoring equilibrium.

Financialisation, once a stabilising mechanism, now amplifies vulnerability. Exporting inflation through reserve currency privilege can delay crisis but cannot indefinitely substitute for productive renewal.

Three Systemic Trajectories

The unfolding US–BRICS confrontation may follow one of three broad trajectories:

1. Escalatory Fragmentation

Military confrontation widens; sanctions proliferate; technological ecosystems bifurcate. Rival blocs consolidate around competing financial and energy architectures. Systemic instability intensifies.

2. Managed Competitive Multipolarity

Rivalry persists but remains bounded. Strategic sectors are securitised, yet economic interdependence survives in modified form. Regional spheres stabilize without total rupture.

3. Negotiated Structural Reform

Global institutions undergo recalibration. IMF voting rights adjust; development finance expands; dollar dependency gradually reduces without systemic collapse.

For the Global South, only the third scenario offers genuine developmental potential. Yet, it requires coordinated agency and strategic autonomy.

After Iran–Venezuela–Syria: Who Is Next?

The question “who is next?” must be understood structurally rather than rhetorically.

States that combine the following characteristics are most vulnerable:

- Significant energy or mineral resources;

- Strategic geographic position along supply corridors;

- Efforts to diversify financial or security alignments beyond Western institutions.

In a world organised around hegemonic transition, geopolitical pressure tends to concentrate where alternative integration threatens established dominance.

Yet, history is not predetermined. Hegemonic transitions have alternated between catastrophic war and negotiated restructuring. The current era unfolds under nuclear overcapacity and ecological crisis—raising the stakes immeasurably.

The Interregnum of the 21st Century

We are living through an interregnum: the old order persists but lacks uncontested legitimacy; the emerging multipolar order remains incompletely institutionalized.

Energy security, technological sovereignty, and monetary architecture have become the decisive arenas of contestation. Military escalation in West Asia intersects with semiconductor controls in East Asia and sanctions policy in Europe.

The erosion of unipolar dominance does not guarantee equitable multipolarity. Multipolarity may reproduce hierarchy under new configurations. The decisive factor will be whether states of the Global South can leverage systemic transition to expand developmental sovereignty rather than become instruments within rival blocs.

Conclusion

The 21st century has witnessed the reassertion of industrial capacity as the decisive foundation of durable geopolitical power. Financial hegemony—once anchored in dollar centrality—now confronts the rise of expansive industrial-technological capability in Asia.

The US–BRICS confrontation reflects a structural contest between finance-capital predominance and productive-industrial ascendancy. Energy corridors, supply chains, currency systems, and digital infrastructure form the battleground of this new era.

Iran, Venezuela, and Syria illustrate how energy geopolitics and sanctions intertwine. The question of “who is next” depends not on rhetorical hostility but on structural positioning within global energy and financial networks.

We are entering a prolonged phase of instability characteristic of hegemonic transition. Whether this transition culminates in fragmentation or negotiated reform will determine the trajectory of the twenty-first century.

The age of uncontested unipolar dominance has ended. What replaces it remains politically open, structurally constrained, and historically consequential.

Table 1: Global Reserve Currency Shares

The writer, an economics professor and author, is currently engaged in research on Sustainable Economic Development, Political Economy of the Global South, and India’s Socioeconomic Crisis. The views are personal. acpuum@gmail.com.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.