Locked Out of My Own Money: Banking on Charges, Not Trust

At the entrance of many Indian bank branches stands a quiet contradiction: a heavy iron gate, chained and padlocked with bureaucratic precision, directly beneath a sign that boldly declares, “Where the Customer Is a King.” The phrase—often attributed to Gandhi ji—is meant to evoke respect and service. Yet here, it hangs above a barrier that quite literally keeps people out. One is left wondering: is this a bank or a fortress? A service institution or a gated republic?

The so-called king must knock. Then wait. And sometimes plead.

Beyond the gate, the cool comfort of the bank awaits—but only after the customer has passed a series of silent, unwritten tests:

-

Can they time their visit to avoid the lunch-hour lockdown?

-

Can they interpret the security guard’s gestures without asking?

-

Can they endure the ritual of “manager is busy, come tomorrow”?

The irony isn’t just in the architecture—it’s in the attitude. That chained gate isn’t about security. It’s a symbol. It says: “We’ll serve you, but only on our terms.” It’s the physical embodiment of a system that speaks of dignity but delivers denial.

And so unfolds the daily ritual at the doorstep of Indian banking—where the customer is a king, but must crawl through the gate.

A Citizen’s Entry Denied: The ₹9,100 That Disappeared

In a country that celebrates Jan Dhan inclusion and digital empowerment, I—an experienced banker and citizen—found myself locked out of my own funds for nearly 300 days. This is not a personal grievance. It is a case study in how digital banking, regulatory ambiguity, and institutional apathy converge to erode customer dignity.

On an ordinary day, I mistakenly transferred ₹9,100 via NEFT from my ICICI Bank savings account to an unintended beneficiary at Bank of India. I contacted ICICI Bank immediately, and was assured that a lien had been placed and a dispute initiated. A service request (SR1018307723) was generated, and I was informed that an indemnity bond had been filed with Bank of India.

What followed was a long and confusing ordeal, marked by silence, delay, and procedural fog:

-

Over 10 personal visits to the branch yielded no progress

-

No written communication was shared regarding the indemnity bond or Bank of India’s response

-

Customer helpline calls on 10.09.2025—at 11:34 AM and 11:48 AM—were abruptly disconnected without resolution

-

Even accessing the branch required adjusting a chain between iron grills—an indignity for any citizen, let alone senior customers

This wasn’t merely a failed transaction—it was a procedural lockout. The episode grew increasingly muddled, forcing me to consider escalation.

The Limits of Digital Recourse

India’s digital banking infrastructure, particularly UPI, has expanded rapidly. But its grievance redressal mechanisms remain fragmented and opaque. Crucially, UPI dispute workflows do not apply to NEFT transactions, leaving customers like me with limited options.

Here’s what the escalation path looks like in practice:

-

Bank-Level Resolution

-

Initiate a service request and indemnity bond

-

Follow up through branch visits and helpline calls

-

In my case, this yielded no written updates or closure

-

-

NPCI Dispute Redressal

-

Not applicable for NEFT transactions

-

Designed primarily for UPI, IMPS, and wallet-based disputes

-

-

RBI Escalation

-

Filing a complaint via the RBI CMS portal is technically possible

-

However, the process is complex, time-bound, and often inaccessible to ordinary citizens without legal guidance

-

-

Consumer Forum

-

The only remaining recourse is to file a formal complaint with the District Consumer Disputes Redressal Commission

-

This requires documentation, time, and legal preparedness—burdensome for a citizen seeking basic redress

Conclusion: A System That Preaches Empowerment but Practices Evasion

This episode exposes a deeper institutional failure. While digital banking promises speed and inclusion, it often delivers silence and exclusion. With no unified grievance redressal framework for NEFT disputes, citizens are left stranded—forced to navigate chains, portals, and procedural haze just to reclaim what is rightfully theirs.

The Vanishing Bank: From Passbooks to Portals

There was a time when a bank was a place—not a portal. You walked in, greeted the teller, deposited your pension, and left with a stamped passbook and a sense of dignity. Today, the bank is a screen. The teller is a chatbot. The passbook is a PDF. And dignity? That’s been debited—along with ₹295 for not maintaining a minimum balance.

This article is not a lament for nostalgia. It is a citizen’s indictment of a system that has replaced trust with terms, service with charges, and inclusion with indifference.

At the heart of this critique lies a paradox: while banks have written off over ₹13 lakh crore in loans over the past decade, they continue to penalize ordinary citizens for falling short of ₹5,000 in their savings accounts. The Ministry of Finance assures us that “Write-off ≠ Waiver,” as if semantics can mop up the moral stain of unrecovered billions. Meanwhile, the citizen pays—not just in rupees, but in dignity.

Anecdote: The Curious Case of Ram Bharose

Ram Bharose, a retired schoolteacher from a small town in Uttar Pradesh, walked into his local bank branch one morning. Or rather, he tried to. The security guard, now upgraded to biometric gatekeeper, informed him that “physical banking is discouraged.”

“Download the app,” he said.

“I use a Nokia,” replied Ram Bharose.

“Then upgrade your banking behaviour.”

Inside, the bank resembled a showroom of slogans—not with customers, but with posters. “Go Digital. Go Paperless. Go Away,” they seemed to say. The chairs were empty, the counters unmanned, and the only sound was the whir of a ceiling fan spinning like the RBI’s circular logic.

Ram Bharose finally reached the help desk, where a young executive explained that his account had been debited ₹295 for “non-maintenance of minimum balance.”

“But I only have ₹3,000,” he protested.

“Exactly,” she replied. “You need ₹5,000 to avoid charges. It’s in the terms and conditions.”

“Where?”

“On the website.”

“I don’t have internet.”

“Then you should upgrade your banking behaviour.”

He left the bank poorer than he entered—not just in rupees, but in dignity.

From Lending Losses to Digital Deductions: The Legal Contradiction of Modern Banking

The Banking Regulation Act, 1949, defines banking under Section 5(b) as:

“Accepting, for the purpose of lending or investment, of deposits of money from the public, repayable on demand or otherwise…”

This definition is functional, not exhaustive. It frames banking as financial intermediation—deposit-taking and lending—but says nothing about penalizing customers for failing to deposit “enough.” There is no statutory basis for charging fees simply because a citizen’s balance falls below a threshold.

Yet today, service charges have become the silent backbone of retail banking. Why?

Between FY2014 and FY2024, Indian banks wrote off over ₹16.6 lakh crore in loans. Public sector banks alone accounted for ₹12 lakh crore. SBI, the largest lender, wrote off ₹1.14 lakh crore in five years.

Recovery? Just ₹2.69 lakh crore—a paltry 16.2%.

Having failed to recover from large borrowers, banks have quietly shifted their revenue model—from interest income to fee extraction. The new strategy? Digitally imposed service charges, deducted automatically from retail accounts.

Digitally Debited, Invisibly Imposed

Over the past decade, banks have embraced fee-based recovery—often through automated digital debits that bypass physical consent and real-time awareness. These charges are not negotiated; they are deducted.

Common service charges now levied digitally include:

-

Non-maintenance of Average Monthly Balance (AMB): ₹150–₹600 per month

-

SMS alert fees: ₹15–₹25 per quarter, even when alerts are disabled

-

ATM usage beyond free limit: ₹20–₹25 per transaction

-

Cheque book issuance: ₹50–₹100 after a limited free quota

-

Cash deposit at non-home branch: ₹50–₹150 per transaction

-

Standing instruction failure: ₹250–₹500 per bounce

-

Debit card annual fees: ₹150–₹750, auto-debited without renewal notice

-

Account closure within 12 months: ₹500–₹1,000 penalty

-

Re-KYC processing or account reactivation: ₹100–₹250 in some banks

-

Dormancy reactivation: Charges applied even when inactivity was due to system freeze

These charges are digitally executed—often without SMS confirmation, email alert, or branch-level explanation. The interface is algorithmic; the impact is human.

Legal Permission vs Moral Justification

The RBI, through its Master Circulars and Charter of Customer Rights (2014), permits banks to levy charges—provided they are transparent, non-discriminatory, and disclosed. But legality is not morality. Just because a charge is permitted does not mean it is justified—especially when it targets the digitally excluded, the elderly, and the economically vulnerable.

The contradiction is stark: banking law defines service as deposit and repayment. Yet today’s banks define service as deduction and penalty—executed through digital rails that many citizens cannot see, question, or resist.

The irony is rich: banks that failed to recover from billionaires now recover from pensioners—one ₹295 deduction at a time.

Digital Banking: A Premium Gate with No Exit

Banks promote digital banking as the future. But for many, it’s a locked gate with no exit:

-

Buggy interfaces and inaccessible language options

-

Chatbots that deflect, not resolve

-

Complaint portals with no escalation path

-

Forced digital migration without physical alternatives

“Digital banking was meant to democratize access. Instead, it has become a premium gate—charging for entry, but failing to deliver dignity.”

Re-KYC and the Freezing Paradox: Digital Punishment Without Due Process

The RBI mandates that banks issue three reminders before freezing accounts due to KYC lapses. Yet in practice, many banks freeze accounts abruptly—without notice, without explanation, and often without fault on the part of the customer. The result is a digital punishment: sudden denial of access to one’s own money, triggered not by fraud or misuse, but by procedural rigidity.

Worse, these actions frequently lack statutory grounding in the RBI Act or the Banking Regulation Act, creating a grey zone of enforcement where compliance overrides compassion.

A missed KYC update should not become a financial death sentence—especially in a system that claims to empower through digitization.

The Role—and Failure—of the Indian Banks’ Association (IBA)

The IBA is meant to:

-

Represent banks in policy discussions

-

Standardize practices across institutions

-

Advocate for customer-centric reforms

-

Coordinate with regulators like RBI and SEBI

But in practice, it has:

Taken no stance on digital exclusion

-

Remained silent on unjust account freezing

-

Failed to engage in public grievance redressal

-

Prioritized institutional convenience over customer dignity

“IBA has become a voice for banks, not for banking.”

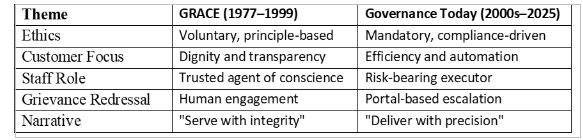

Historical Ethics: GRACE vs Governance – A Comparative Lens

In 1977, the IBA introduced GRACE—Ground Rules and Code of Ethics. It wasn’t enforceable, but it was a moral compass. GRACE asked banks to serve transparently and operate with dignity.

“GRACE was never about regulation. It was about reputation.”

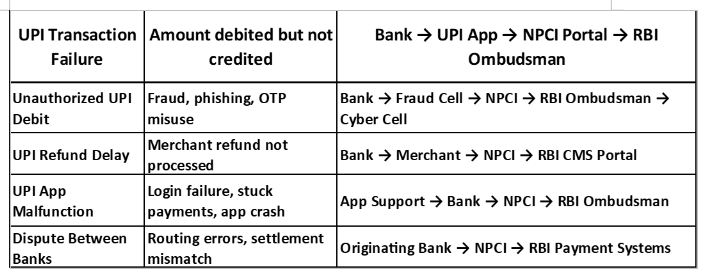

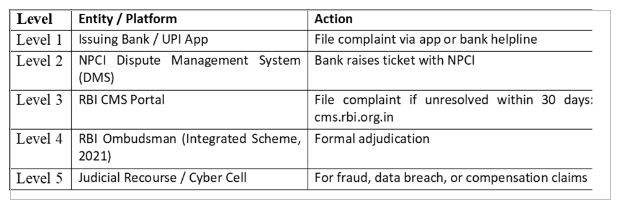

NPCI & UPI Dispute Redressal Workflow

India’s digital banking infrastructure, particularly UPI, has grown rapidly — but its grievance redressal remains fragmented and opaque. Here’s a structured table mapping common issues and escalation paths:

UPI Dispute Redressal Workflow

NPCI Grievance Escalation Channels

Observation: These workflows are technically sound but practically inaccessible to many — especially senior citizens, rural users, and those without digital fluency.

The Architecture of Indignity

The physical design of many bank branches mirrors their operational dysfunction:

Chained iron gates at the entrance

-

No privacy at counters

-

Elderly customers standing in queues with no seating

-

Staff shouting across counters to manage crowd control

All this under a signboard that reads “Where the Customer Is King.” The irony is architectural. The gate isn’t just a barrier — it’s a metaphor.

Case Example:

A senior citizen was seen adjusting a chained gate to squeeze into a branch. Inside, he was asked to return with “correct documents,” despite being a nominee on a deceased account. The staff, under pressure to manage crowd and compliance, had no time to explain RBI’s simplified nominee norms.

Conclusion: When senior citizens must negotiate metal barriers to reach a teller, it’s not just a design flaw — it’s a democratic failure.

Democracy in Disrepair

A democracy is not just about voting rights or constitutional guarantees — it’s about access, respect, and inclusion in daily civic life. When citizens must physically adjust a chain between iron grills to enter a bank, it reflects:

-

Institutional neglect: Absence of basic infrastructure for ease and dignity

-

Symbolic exclusion: A barrier — literal and figurative — between citizens and services

-

Power asymmetry: The bank appears fortified while the customer is made to feel like an outsider

“In a democracy, access to public services should never feel like trespassing.”

Final Reflection: Toward a Dignified Banking Architecture

India’s banking future must be built not just on apps and algorithms, but on access, empathy, and accountability.

Reform Must Begin with:

-

Guaranteed physical access for all customers

-

Transparent, time-bound complaint resolution

-

RBI activism anchored in statutory clarity

-

IBA restructured to include consumer representation

-

Digital platforms made optional, not coercive

“We don’t need more charges. We need more choices.”

“A democracy that digitizes its banks must not dehumanize its citizens.”

The author is a CAIIB (Certified Associate of the Indian Institute of Banking and Finance), has 37 years of work experience in the private sector and in a nationalised bank, and is the All India Deputy General Secretary of the All India Bank Officers’ Confederation.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.