How RBI’s Rules Locked ₹67,000Cr Citizens’ Money in Inoperative, Dormant A/cs

“I hadn’t touched that account in years,” said a retired schoolteacher from Kanpur. “But it had my pension savings. One day, I tried to withdraw money—and the bank said my account was inoperative. I didn’t even know what that meant.”

Across India, millions of citizens—senior citizens, migrant workers, bereaved families, and digitally excluded users—have faced similar shocks. Their accounts, often holding life savings or government benefits, are quietly locked. Not due to fraud. Not due to error. But due to a regulatory label: “inoperative.”

In India’s banking system, silence is treated as suspicion. If a savings or current account shows no customer-initiated activity for 24 months, it is classified as inoperative. This triggers a cascade of restrictions: digital access is blocked, interest may stop accruing, and reactivation demands fresh KYC (Know Your Customer)—even if the account was previously verified.

This article traces the hidden pipeline from inoperative classification to the DEA (Depositor Education and Awareness) Fund, critiques the logic behind it, and proposes reforms to restore dignity, transparency, and trust.

RBI’s Dormancy Framework — A Rule Without Reason

The RBI’s 2024 and 2025 circulars define dormancy with precision but little empathy. An account is deemed inoperative if it shows no customer-initiated transactions for 24 consecutive months. This includes savings, current, Jan Dhan, and fixed deposit accounts.

What counts as activity

-

Cash deposits or withdrawals

-

Cheque issuance or clearing

-

Fund transfers (NEFT, IMPS, RTGS)

-

ATM, UPI, or mobile banking

-

Non-financial actions like KYC updates or balance inquiries

What Doesn’t Count

-

Interest credits

-

Charges, fees, penalties

-

Standing instructions executed by the bank

-

Auto-renewal of fixed deposits

Even if an account earns interest or receives automatic credits, it can still be classified as inoperative unless the customer actively interacts with it. The framework is applied uniformly, regardless of account type, balance, or context. It treats silence as abandonment, ignoring the realities of passive saving, bereavement, or digital exclusion.

Public Impact — Disruption Without Fault

For ordinary citizens, the term “inoperative account” is not just a technical label—it’s a sudden disruption of financial access.

Anecdotal Glimpse

Sunita Verma, a homemaker in Bhagalpur, discovered her bank account was “inoperative” when her UPI (Unified Payments Interface) transaction failed. Her LPG subsidy didn’t arrive. At the bank, she was told to redo her KYC—despite having done it last year. “Is my money gone?” she asked. No one had warned her. No one explained.

Dormancy Triggered Without Warning

Across India, thousands of savings accounts are routinely marked “inoperative” due to inactivity—often without fault, and without prior notice. Despite RBI’s 2024 mandate for pre-dormancy alerts, many banks fail to inform citizens. The result: sudden exclusion from the financial ecosystem.

Consequences

-

Digital Access Blocked: UPI, ATM, mobile banking, and internet banking are disabled.

-

Interest Earnings Halted: Passive income lost despite balances.

-

Government Benefits Disrupted: Direct Benefits Transfers-linked accounts wrongly tagged.

-

Reactivation Burden: Fresh KYC required—even for verified accounts.

-

No Pre-Dormancy Alerts: Despite RBI’s 2024 mandate, many banks fail to notify.

-

Misinterpretation as Forfeiture: Citizens assume their money is lost.

-

Exclusion from Financial Ecosystem: Auto-debits and standing instructions blocked.

-

No Public Awareness Campaigns: RBI and banks have not launched sustained efforts.

Real-World Scale

-

₹67,000+ crore lies unclaimed in RBI’s DEA Fund

-

23% of Jan Dhan accounts are inoperative—affecting over 11 crore citizens

-

Thousands of accounts classified monthly, often without fault

The Inoperative Pipeline — From Silence to Erasure

Dormancy is not a sudden event—it’s a slow drift into invisibility. It begins with silence, deepens through procedural rigidity, and ends in institutional disengagement. This journey can be traced through a hidden pipeline:

The Pipeline Flow: Inoperative → Dormant → DEA Fund → Forgotten.

-

Inoperative: After 24 months of no customer-initiated activity, an account is classified as inoperative. Digital access is blocked. Interest may stop. Reactivation demands fresh KYC—even for verified accounts.

-

Dormant: If the account remains untouched for 10 years, it is deemed dormant. The depositor is rarely alerted. Outreach is inconsistent. Many citizens remain unaware of the impending transfer.

-

DEA Fund Transfer: The account balance is quietly moved to RBI’s DEA Fund. The funds vanish from the customer’s account view. There is no opt-in dashboard, no consent mechanism, and no audit trail of successful claims.

-

Forgotten: Without proactive tracing, the money remains locked. Citizens lose visibility. Families lose access. The system treats silence as abandonment, not as a signal to engage.

Read Also: Locked Out of My Own Money: Banking on Charges, Not Trust

In Bhubaneswar, a retired railway worker stood at the bank counter, confused and upset. His account had been blocked, and his money quietly moved to the RBI’s DEA Fund. No one had warned him. “It’s policy,” the bank clerk said. “But I didn’t leave it,” the man replied. His words speak for many others who are treated as if silence means they’ve given up—when really, they’ve just been left out.

The DEA Fund — Stockpile of Forgotten Ownership

Imagine this: a citizen opens a savings account, deposits funds, and lets it sit untouched—perhaps due to migration, bereavement, or simply passive saving. Years pass. No alerts arrive. No reminders are sent. Eventually, without consent or visibility, the balance is transferred to a fund they’ve never heard of: the Depositor Education and Awareness (DEA) Fund, managed by the Reserve Bank of India.

This fund was created to hold unclaimed deposits after 10 years of inactivity. It includes balances from savings accounts, fixed deposits, recurring deposits, demand drafts, and pay orders. Once transferred, the money disappears from the customer’s account view. There is no dashboard. No opt-in mechanism. No audit trail of successful claims.

How much public money is locked away? The numbers raise more questions than answers:

-

RBI’s own Annual Report (March 2024) shows ₹78,213 crore parked in the DEA Fund — money from unclaimed deposits.

-

Media reports (June 2025) estimate the figure at ₹67,000+ crore — a noticeable gap.

-

Experts speculate that if you include both dormant and inoperative accounts, the total could be ₹2 to ₹3.5 lakh crore.

-

Yet RBI has never publicly explained the difference between “inoperative” and “dormant” accounts — leaving citizens confused about what qualifies, and what’s recoverable.

To help citizens locate unclaimed deposits, the RBI launched the UDGAM portal in 2023. It was a welcome step—but only a partial one.

UDGAM currently covers around 90% of institutions linked to the DEA Fund. Citizens can search using their name and partial address, but key identifiers like PIN code, PAN, or account number are not supported. These limitations make it difficult for many to find their own funds—especially those with common names or incomplete records.

Even when a match is found, the process stalls. There’s no way to track the status of a claim, no data on how much money has been successfully returned, and no central dashboard to monitor progress. The portal offers discovery—but not resolution. Visibility ends where accountability should begin.

Reformist Insight: The DEA Fund is not just a financial reserve—it’s a record of forgotten ownership. And until that record is made transparent and traceable, citizen trust will remain trapped in layers of procedure and silence.

Jan Dhan — Inclusion Meets Institutional Neglect

The Jan Dhan Yojana was launched to promote financial inclusion. Yet under RBI’s dormancy framework, even these accounts—often linked to government benefits—are vulnerable.

As of 2025, nearly 23% of Jan Dhan accounts are classified as dormant. These include accounts receiving DBT, pensions, scholarships, and subsidies. RBI has directed banks to exclude DBT-linked accounts from dormancy classification, but compliance remains inconsistent.

Many recipients never used these accounts beyond the initial credit. Without alerts or outreach, their accounts drift into inoperativeness. Reactivation demands fresh KYC—often beyond their digital or geographic reach.

Dormancy penalises trust, not abandonment. The very accounts meant to empower the vulnerable become inaccessible through procedural rigidity.

Double Trouble: Dormancy Followed by Redundant KYC

Inoperative classification doesn’t just block access—it creates a two-stage burden for citizens.

The first trouble: Needlessly marked inoperative

accounts are classified as inoperative after 24 months of no customer-initiated activity—even if they continue to earn interest or receive automatic credits. This rigid framework treats silence as abandonment, ignoring life transitions, passive saving, or digital exclusion.

The second trouble: Redundant KYC for reactivation.

Once an account is marked inoperative, reactivation requires fresh KYC—even if the account was previously verified and flagged as “safe.” RBI’s 2024 directions allow reactivation at any branch or via video customer identification process (V-CIP), subject to bank capability. No charges may be levied, and the process must follow a maker-checker protocol.

Yet in practice:

-

Citizens are asked to revisit home branches

-

Redundant documents are demanded

-

Digital channels are opaque and inconsistent

The contradiction is stark: the system demands re-verification of accounts that it already trusts. This is not risk-mitigation, it’s operational inertia.

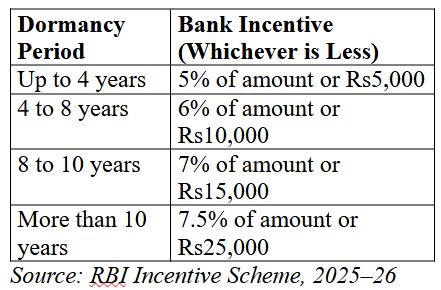

RBI’s Incentive Scheme — A Reactive Patch

In 2025–26, the RBI introduced a financial incentive scheme to encourage banks to trace and reactivate dormant accounts. The idea was to promote restitution by rewarding institutions that help restore citizen access to long-forgotten funds.

Depending on the deposit amount and the duration of dormancy, banks can earn up to ₹25,000 per account reactivated:

While the scheme appears citizen-friendly, it reveals a deeper contradiction in RBI’s dormancy framework.

RBI itself mandates dormancy after just two years of inactivity—often without fault, warning, or proactive outreach. Then, years later, it pays banks to restore access to those same accounts, without addressing the root causes of disengagement.

This setup encourages banks to act only after dormancy has set in—blocking accounts, transferring balances, and eventually moving funds to the DEA Fund—rather than helping citizens stay active and informed from the start. It gives incentives for post-facto action, instead of building safeguards that prevent exclusion.

In effect, RBI’s framework first propagates inoperativeness, then rewards its reversal. The increase in dormant accounts is not accidental—it’s a structural outcome of early classification, procedural opacity, and lack of citizen engagement.

If RBI genuinely seeks financial inclusion, it must first reform its own dormancy architecture. The two-year trigger should be re-evaluated, and citizen-centric safeguards must be built in—such as proactive alerts, opt-in dashboards, and simplified reactivation pathways.

The RBI’s current approach creates the very exclusion it later pays banks to undo. Preventing dormancy is more ethical—and more efficient than rewarding institutions for restoring access to accounts that were sidelined by design.

Reform-Oriented Questions for RBI

-

Why is dormancy triggered after 24 months, even for verified accounts with passive savings?

-

Why are citizens not alerted before dormancy classification or DEA transfer?

-

Why must verified users undergo full KYC reactivation?

-

Why is the DEA Fund not searchable by account number, or PAN?

-

Why are DBT-linked Jan Dhan accounts still marked dormant?

-

Why does RBI pay banks to reverse dormancy it mandates?

-

Why is there no unified dashboard showing restitution outcomes?

Reform begins not with answers, but with the courage to ask

Reform Proposals —Compliance and Compassion

To rebuild public trust and make banking rules easier to understand and follow, RBI and other institutions need to take action that puts citizens first. The changes suggested here aren’t just small fixes, they’re essential. They aim to shift the framework from suspicion to support, from opacity to ownership, and from remediation to prevention.

Key Proposals

-

Extend Dormancy Threshold

-

Raise the inactivity window from 24 months to 5 years, especially for verified accounts.

-

Align with global best practices (e.g., the US: 5 years; the UK: 15 years).

-

Recognise that silence may reflect life transitions—not abandonment.

-

-

Mandate Pre-Dormancy Alerts and Nominee Outreach

-

Enforce RBI’s 2024 circular requiring SMS, email, or physical letters before dormancy classification.

-

Require banks to contact nominees or legal heirs before DEA Fund transfer.

-

Publish compliance metrics and penalise non-adherence.

-

-

Recognise Auto-Renewal of FDs as Valid Activity

-

Treat auto-renewal of fixed deposits as customer engagement, not inactivity.

-

Prevent linked savings accounts from being penalised for passive investment behaviour.

-

-

Simplify Reactivation for Verified Accounts

-

Enable reactivation via mobile apps or Aadhaar-linked OTP for accounts already marked “safe.”

-

Remove redundant KYC unless risk is flagged.

-

Allow reactivation at any branch, not just home branch.

-

Ensure V-CIP is available across banks, with no charges.

-

Retain maker-checker audit logs and send post-reactivation alerts.

-

-

Strengthen UDGAM and Bank-Level Searchability

-

Enable search by account number, or PAN, not just name and partial address.

-

Require banks to host searchable DEA deposit lists on websites and branches, updated monthly.

-

Add claim tracking, opt-in alerts, and publish restitution success metrics.

-

-

Audit Jan Dhan Segregation

-

Enforce RBI’s directive to exclude DBT-linked accounts from dormancy classification.

-

Penalise banks that fail to segregate vulnerable accounts.

-

Publish compliance audits and corrective actions.

-

-

Publish Dormancy and DEA Metrics

-

Release public data on:

-

Monthly dormancy classifications

-

Reactivation volumes

-

Funds returned from DEA Fund

-

Bank-wise performance under the incentive scheme

-

-

Create a central dashboard for transparency and citizen awareness.

-

-

Reframe Incentive Logic

-

Shift from reactive payouts to preventive engagement.

-

Reward banks for maintaining active citizen contact—not just tracing lost accounts.

-

Link incentives to outreach success, not just account recovery.

-

-

Enforce Quarterly Outreach and Tracing Protocols

-

Require banks to contact holders of inoperative accounts every quarter via letters, SMS, or email.

-

If contact fails, mandate tracing via introducers, nominees, or legal heirs.

-

Publish audit logs of outreach attempts and tracing outcomes.

These reforms must now move from policy suggestion to institutional execution. RBI should issue updated circulars to operationalise these proposals, with clear timelines, compliance audits, and public dashboards. Banks must embed these protocols into their core systems—not as exceptions, but as defaults.

Beyond Compliance — A Call to Stakeholders

Reform cannot remain the RBI’s internal housekeeping. It must become a public mandate—a shared responsibility across institutions, professions, and citizens. Dormancy is not just a regulatory status, rather it is a symptom of systemic disengagement. The current framework penalises silence without understanding its cause. Citizens lose access, visibility, and dignity. Deposits vanish into the DEA Fund, and reactivation becomes a bureaucratic maze.

This must change—and it begins now. Stakeholders must act.

-

Banks must stop hiding behind compliance checklists. They must send timely alerts, simplify reactivation, and publish monthly restitution metrics. Every inoperative account must trigger outreach—not silence.

-

Journalists must investigate dormancy trends, expose gaps in implementation, and amplify citizen voices. The ₹67,000 crore in the DEA Fund is not just a number—it’s a national story waiting to be told.

-

Civil society organisations must launch awareness drives, legal clinics, and multilingual toolkits to help citizens reclaim their deposits. Dormancy must be treated as a public rights issue—not a technical footnote.

-

Legal institutions must scrutinise procedural overreach, enforce depositor rights, and ensure that dormant funds are not lost to opacity. Every blocked account deserves judicial clarity.

-

Citizens must stop waiting for reform. They must:

-

Check their account status regularly

-

Demand alerts from their banks

-

Use UDGAM to trace dormant deposits

-

File written requests for reactivation

-

Share their stories publicly to build pressure

-

Join local or online forums to track restitution outcomes

Dormancy is not a crime. Inactivity is not intent. But silence from institutions must now meet noise from citizens. Reform begins when every depositor becomes a watchdog—and every forgotten account becomes a reason to act.

The author is a CAIIB (Certified Associate of the Indian Institute of Banking and Finance), has 37 years of work experience in a private and a nationalised bank. He is All India Deputy General Secretary of the All-India Bank Officers’ Confederation.

Get the latest reports & analysis with people's perspective on Protests, movements & deep analytical videos, discussions of the current affairs in your Telegram app. Subscribe to NewsClick's Telegram channel & get Real-Time updates on stories, as they get published on our website.